Search

Search

Mortgage Basics - Glossary of Terms

Mortgage Term - The period of time your mortgage agreement will be in effect, including your interest rate and terms and conditions. At the end of the term, you may either pay off the mortgage in full, renew it or possibly renegotiate your mortgage agreement (for example, decrease your amortization period). Terms are generally for six months to 5 years.

Open Mortgage - A mortgage which can be prepaid at any time, without requiring the payment of additional fees. Due to the added flexibility of open mortgages, generally the interest rate charged for this type of mortgage is higher.

Closed Mortgage - A mortgage agreement that cannot be prepaid, renegotiated before maturity. Interest rates for closed mortgages are generally lower than open mortgages, which may make them a better choice if payout is not expected in the short term.

Fixed Rate Mortgage - A mortgage for which the rate of interest is fixed for a specific period of time (the term). Payments are set in advance for the term. This provides you with the security of knowing precisely how much your payment will be throughout the mortgage term. Fixed rate mortgages can be open (may be paid off at any time without penalty) or closed (prepayment penalties may apply if paid off prior to maturity).

Variable Rate Mortgage - A mortgage for which the rate of interest can change if other market conditions change. This is sometimes referred to as a "floating rate" mortgage. If interest rates go down, more of the payment is applied to reduce the principal; if rates go up, more of the payment is applied to payment of interest. Variable rate mortgages may be open or closed.

Conventional Mortgage - A mortgage that does not exceed 80% of the purchase price of the home. Mortgages that exceed this limit must be insured against default and are referred to as a high-ratio mortgage.

High-Ratio Mortgage - If you do not have 20% of the lesser of the purchase price or appraised value of the property, your mortgage must be insured against payment default by a mortgage insurer, such as CMHC.

CMHC (Canada Mortgage and Housing Corporation) - Mortgage insurance insures the lender against loss in case of default by the borrower. Mortgage insurance is provided to the lender and the premium is paid by the borrower.

Foreclosure - A legal procedure whereby the lender obtains ownership of the property following default by the borrower by terminating all of the borrower's rights in the property covered by the mortgage.

Amortization - An amortization period means the number of years you will need to pay off your entire mortgage. It is an important decision that can affect how much interest is paid over the life of your mortgage. Historically, the average amortization period for mortgages was 25 years.

The following table illustrates the interest cost over different amortization periods on a $150,000 mortgage, assuming a constant annual interest rate of 5.45%.

| Mortgage Amount | Amortization | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| $150,000 | 25 years | $911 | $123,368 |

| $150,000 | 20 years | $1,022 | $95,391 |

| $150,000 | 15 years | $1,217 | $69,027 |

| $150,000 | 10 years | $1,620 | $44,360 |

NOTE: The amortization period you select can be re-evaluated every time you renew your mortgage.

Prepayment Penalty

A fee charged when a borrower retires a mortgage loan before its scheduled payoff date or maturity.

How is the Prepayment Penalty Calculated?

The prepayment penalty methods below are common methods used by financial institutions. It is important you review and speak to your credit union about your specific mortgage agreement to determine how a mortgage pre-payment penalty will be calculated.

Two common methods used to calculate a prepayment penalty are as follows:

- Three Month Interest Penalty - An amount equal to three months' interest on your outstanding mortgage balance.

- Interest Rate Differential (IRD) - The difference between the interest payable on your existing mortgage versus the interest rate payable on a replacement mortgage for the remaining amount of time left in the mortgage term. The penalty amount is based on the difference between two interest rates. The first is the interest rate for your existing mortgage term. The second is today's interest rate for a term that is similar in length to the time remaining on your existing term. Please note, some financial institutions use a discount interest rate off their posted interest rate when they set up the mortgage term. The discount rate may be used to determine the IRD.

For example, if you have three years left on a five year term, your lender would use the interest rate it is currently offering for a three year term to determine the second rate for comparison in the calculation.

Your mortgage contract may state that the prepayment penalty will be the greater of the two amounts that result from the calculations used above.

Examples of the two most common methods of pre-payment penalty calculations are as follows:

Method 1: Three months' interest:

To estimate a penalty based on three months' interest, we can use this formula:

A x B ÷ 12 months x 3 months

A = Outstanding mortgage balance

B = Annual interest rate

| STEP | AMOUNT |

|---|---|

| Step 1: Identify the outstanding balance on the mortgage | $200,000 |

| Step 2: Multiply the outstanding mortgage balance (A) by the annual interest rate (B) | $200,000 x 0.06 = $12,000 |

| Step 3: Divide the answer by the months to get the amount of interest payable for one month | $12,000 ÷ 12 = $1,000 |

| Step 4: Multiply the answer by 3 months | $1,000 x 3 = $3,000 |

| Pre-payment charge estimate based on three months' interest is | $3,000 |

Method 2: Interest Rate Differential (IRD):

To estimate the prepayment penalty based on the interest rate differential (IRD), we can use this formula (this is one way to complete the calculation. However calculation methods may vary by financial institutions.):

A x (B - C) ÷ 12 months x D

A = Outstanding mortgage balance

B = Annual interest rate

C = Today's interest rate for term of similar length. Note: the lender may round up or down to the nearest term

D = Number of months left in term

| STEP | AMOUNT |

|---|---|

| Step 1: Identify the annual interest rate on the mortgage (B) | 6% |

| Step 2: Identify today's interest rate for a term that is similar in length to the time left in the term (C) - (currently 4% for a 3 year term) | 4% |

| Step 3: Subtract the answer from Step 2 from the answer in Step 1 to get the difference in interest rates (B - C) | 6% - 4% = 2% or 0.02 |

| Step 4: Multiply this answer by the outstanding mortgage balance (A) to get the interest differential for one year | 0.02 x $200,000 = $4,000 |

| Step 5: Divide this answer by 12 months to get the interest differential for one month | $4,000 ÷ 12 = $333.33 |

| Step 6: Mulitply this answer by the number of months left in the term (D) - (36 months) | $333.33 x 36 = $12,000/td> |

| Prepayment charge estimate based on IRD: | $12,000 |

Prepayment Privileges

How can I reduce or avoid prepayment penalties and still pay off my mortgage quickly?

- Make full use of your prepayment privileges: Prepay as much as you are allowed within your mortgage contract each year. Make sure you are clear on what your mortgage contract will allow you to prepay and take full advantage of it. The interest savings can make a significant difference.

- Wait until the end of your term to prepay: If your prepayment penalty will be a large amount, consider waiting until the maturity date, when you can make a lump sum prepayment without triggering penalties.

- Ask Questions: Ask your credit union Account Manager for suggestions on how you can pay your mortgage down quicker. There may be opportunities to make lump sum payments, increase regular payments or change your payment frequency.

Contact us with any questions about your mortgage - 306.228.2688.

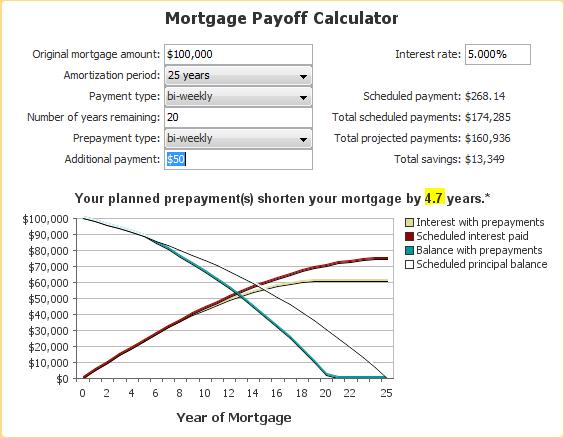

Prepayment Savings

Sample of a mortgage with accelerated payments of an additional $50.00 bi-weekly.

Interest Saved - $13,349

Years shortened - 4.7 years